Home

/ How To Calculate Sharpe Ratio : The formula is pretty simple, and intuitive:

How To Calculate Sharpe Ratio : The formula is pretty simple, and intuitive:

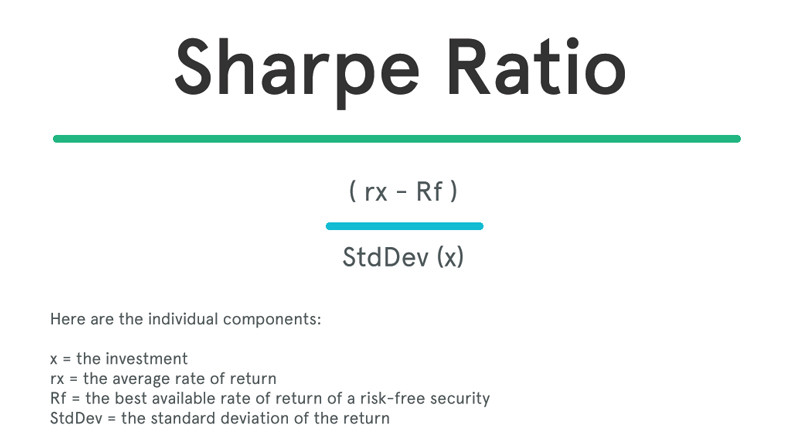

How To Calculate Sharpe Ratio : The formula is pretty simple, and intuitive:. I know this sounds complicated, so let's take a look at it and break it down. Here is the standard sharpe ratio equation: Sharpe ratio formula the sharpe ratio formula is calculated by dividing the difference of the best available risk free rate of return and the average rate of return by the standard deviation of the portfolio's return. The result is then divided by the fund's standard deviation. If there are n trading periods in a year, the annualised sharpe is calculated as:

Sharpe ratio of 2 or more is considered as good comparing to majority of the fund performance out there. The information derived from the sharpe ratio calculation can be used for various purposes: With a sharpe ratio of 3 or more makes you a star in the financial industry. Uses of the sharpe ratio. The sharpe ratio is the most popular formula for calculating risk adjusted returns.

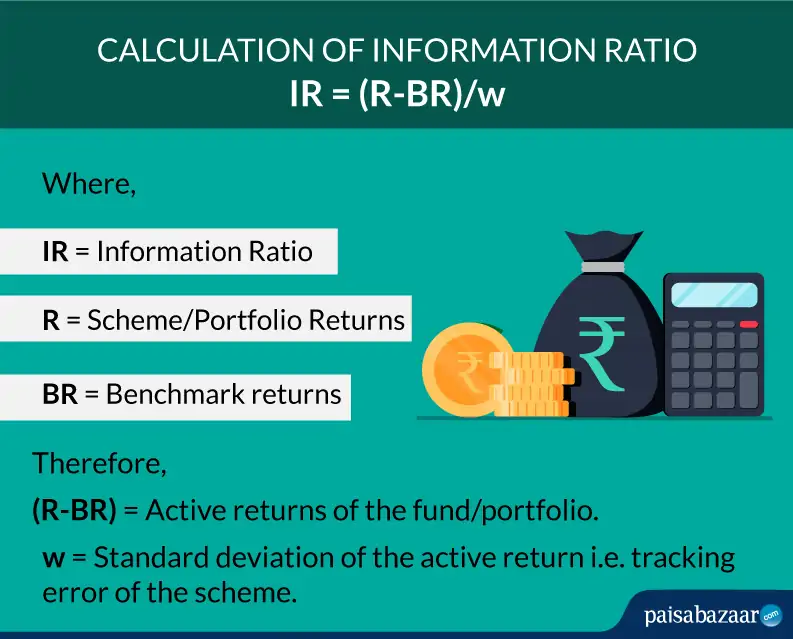

How To Calculate Information Ratio Sharpe Ratio Vs Information Ratio from www.paisabazaar.com Treasury bond yields as a proxy. The sharpe ratio measures the excess return for taking on additional risk. Suppose you are asked to find the sharpe ratio of a fund which has a 30% portfolio return a 10% free risk return and a 15 standard deviation of portfolio return. For my example, the formula would be =stdev (d5:d16) finally calculate the sharpe ratio by dividing the average of the exess return by its standard deviation (in my example this would be =d18/d19) vba for the sharpe ratio Divide this value by the standard deviation of the portfolio returns, which can be found using the =stdev formula. A sharpe ratio greater than 1 is considered the baseline for a good investment. Now it's time to calculate the sharpe ratio. As a general rule, anything above 2 is very good, while above 3 is excellent.

Suppose you are asked to find the sharpe ratio of a fund which has a 30% portfolio return a 10% free risk return and a 15 standard deviation of portfolio return.

Calculate sharpe ratio the final step to calculating the sharpe ratio in excel is to divide the average returns by standard deviation. Therefore, the sharpe ratio of the fund is 1.33. The information derived from the sharpe ratio calculation can be used for various purposes: I have a pairs strategy that i am trying to calculate the sharpe ratio for. The more risky an asset, the higher reward an investor should receive and the higher the sharpe ratio will be. Here is the standard sharpe ratio equation: The sharpe ratio is an analysis ratio that compares an investment's returns to its risk. Suppose you are asked to find the sharpe ratio of a fund which has a 30% portfolio return a 10% free risk return and a 15 standard deviation of portfolio return. It allows us to use mathematics in order to quantify the relationship between the mean daily return and then the volatility (or the standard deviation) of daily returns. Jetzt eine riesige auswahl an gebrauchtmaschinen von zertifizierten händlern entdecken Currently i am using python for my analysis and calculation. Below is a summary of the exponential relationship between the volatility of returns and the sharpe ratio. Now it's time to calculate the sharpe ratio.

The sharpe ratio is used to characterize how well the return of an asset compensates the investor for the risk taken, the higher the sharpe ratio number the better. The calculation of sharpe ratio is based on the periodic changes of the asset value and the statistical variation of this periodic change. Now it's time to calculate the sharpe ratio. Currently i am using python for my analysis and calculation. Calculate sharpe ratio the final step to calculating the sharpe ratio in excel is to divide the average returns by standard deviation.

Sharpe Ratio Calculating The Effectiveness Of A Trading Strategy Liteforex from cdn.litemarkets.com The sharpe ratio is an analysis ratio that compares an investment's returns to its risk. Below is a summary of the exponential relationship between the volatility of returns and the sharpe ratio. Remove from the expected portfolio return, the rate you would get from a risk free investment. When it comes to strategy performance measurement, as an industry standard, the sharpe ratio is usually quoted as annualised sharpe which is calculated based on the trading period for which the returns are measured. I have a pairs strategy that i am trying to calculate the sharpe ratio for. The standard deviation of the exess return. Alternatively, depending on the version of excel For my example, the formula would be =stdev (d5:d16) finally calculate the sharpe ratio by dividing the average of the exess return by its standard deviation (in my example this would be =d18/d19) vba for the sharpe ratio

Email me at help@plusacademics.orgthis video give step by step method of how to calculate sharpe ratio using excel.

I am confused on how to convert this information into something that i can calculate the sharpe ratio from. Here is the standard sharpe ratio equation: Divide this value by the standard deviation of the portfolio returns, which can be found using the =stdev formula. For my example, the formula would be =stdev (d5:d16) finally calculate the sharpe ratio by dividing the average of the exess return by its standard deviation (in my example this would be =d18/d19) vba for the sharpe ratio Alternatively, depending on the version of excel The sharpe ratio is the most popular formula for calculating risk adjusted returns. The result is then divided by the fund's standard deviation. Helping to make objective comparison of assets for investment is one of the primary applications of the sharpe ratio. Now it's time to calculate the sharpe ratio. We get the ratio = 12.09% / 8.8% = 1.37x advantages of using sharpe ratio The more risky an asset, the higher reward an investor should receive and the higher the sharpe ratio will be. Sharpe ratio is calculated by dividing the difference between the daily return of sundaram equity hybrid fund and the daily return of 10 year g sec bonds by the standard deviation of the return of the hybrid fund. The calculation of sharpe ratio is based on the periodic changes of the asset value and the statistical variation of this periodic change.

How is the sharpe ratio calculated? Helping to make objective comparison of assets for investment is one of the primary applications of the sharpe ratio. Suppose you are asked to find the sharpe ratio of a fund which has a 30% portfolio return a 10% free risk return and a 15 standard deviation of portfolio return. Sharpe ratio formula the sharpe ratio formula is calculated by dividing the difference of the best available risk free rate of return and the average rate of return by the standard deviation of the portfolio's return. Here is the standard sharpe ratio equation:

Sharpe Ratio Formula Analysis Example Calculation Explanation from www.myaccountingcourse.com It allows us to use mathematics in order to quantify the relationship between the mean daily return and then the volatility (or the standard deviation) of daily returns. This video is part of the udacity course machine learning for trading. We get the ratio = 12.09% / 8.8% = 1.37x advantages of using sharpe ratio Email me at help@plusacademics.orgthis video give step by step method of how to calculate sharpe ratio using excel. I have a dataframe that contains the cumulative returns in $'s for each day. If you are trading for yourself, replace the word fund with you. Therefore, the sharpe ratio of the fund is 1.33. Sharpe ratio is calculated by dividing the difference between the daily return of sundaram equity hybrid fund and the daily return of 10 year g sec bonds by the standard deviation of the return of the hybrid fund.

Sharpe ratio of 2 or more is considered as good comparing to majority of the fund performance out there.

Therefore, the sharpe ratio of the fund is 1.33. Below is a summary of the exponential relationship between the volatility of returns and the sharpe ratio. Uses of the sharpe ratio. With a sharpe ratio of 3 or more makes you a star in the financial industry. A sharpe ratio greater than 1 is considered the baseline for a good investment. It allows us to use mathematics in order to quantify the relationship between the mean daily return and then the volatility (or the standard deviation) of daily returns. If you are trading for yourself, replace the word fund with you. Jetzt eine riesige auswahl an gebrauchtmaschinen von zertifizierten händlern entdecken Currently i am using python for my analysis and calculation. Email me at help@plusacademics.orgthis video give step by step method of how to calculate sharpe ratio using excel. As a general rule, anything above 2 is very good, while above 3 is excellent. The sharpe ratio, named after william forsyth sharpe, is a measure of the excess return (or risk premium) per unit of risk in an investment asset or a trading strategy. The information derived from the sharpe ratio calculation can be used for various purposes:

{kind=link}